Robinhood: A New Generation, A New Bull Market

Written by Kryptonite, 6-11-23

State of the Stock

Robinhood’s time in the stock market has been an arduous one and not one without controversy. The stock went public in a hotly anticipated IPO at about $36.41 on July 29th, 2021. It saw tremendous interest in the first week of trading reaching an overly lofty value at ~$85 a share before starting to sell off. This sell off has relentlessly continued and in many places, you will find negative commentary on the stock.

I personally believe that the stock’s price action bottomed on June 17th, 2022 at about $6.84 a share. Since then the stock has been slowly plodding along and striking higher lows, which I will illustrate later in the charting.

I also believe that the stock’s story is close to turning around and could get more positive attention in the later half of this year. I am going to talk about the balance sheet, cost cutting, charts, and the controversy.

I will be limiting my comments on the balance sheet to lines that I believe deserve notice. For this post, I will be comparing Robinhood to their old school rival, Charles Schwab.

The Balance Sheet

Overall, I read Robinhood’s balance sheet as being quite strong. Particularly in the amount of cash and short term investments that the company is carrying. At 5.46 Billion in cash and 1.52 Billion in short term investments the company can cover operating expenses (excl. COGS) for about 3.5 years.

The company has also shared that the short term investments are in <1 year term treasuries. Which is quite a good decision given the current rates. I only wish they had purchased a little more than 500 million or so.

As of this writing (6-11-23), Robinhood carries a market cap of ~$8.5 billion as well. Their cash position is nearly the size of their entire equity. In comparison, $SCHW (Charles Schwab) has about $75 billion in cash and a market cap of 100 Billion. I believe that the market is underestimating how Robinhood can deploy that cash.

Lastly, Robinhood is very close (9.41 market) to their book value per share (7.83). In comparison, $SCHW has a book value per share of 15.36 and is trading at 55.0 in the market. I believe this illustrates that Robinhood is quite cheap, even after the June ’22 bounce when it was cheaper than the book.

Next, the cashflow at Robinhood is quite good and turned positive in Q4’22. Whereas their rivals are experiencing negative free cash flow during this same period. Robinhood, on a relative basis for this metric, looks to be outperforming during the banking crisis.

During their earnings calls they have also reported a net increase in deposits as well as assets under custody (AUC) increasing by an impressive 26% due to the run on stocks in 2023.

What I find most interesting about this is that customer cash in Robinhood has steadily grown to $11 billion from $2 billion at IPO. It has been on an impressive path of growth. I believe this is the result of their strong “Brokerage Cash Sweep” program and the rates they’ve been able to offer.

They have been able to effectively remove the friction between treasury yield and their customers. This also creates a beneficial situation where their clients can deploy capital quickly, while maintaining some yield from their cash. Effectively, creating productive reserves for their customers who can choose to deploy it at any moment right on their app.

Lastly, the company itself is quite close to profitability. The next 4 quarters are projected by broader WallStreet to come in at an EPS of about -0.01 to -0.03. Any positive change in their costs or earnings could lead to a surprise profit. Such as cash from treasury yield, cost cutting measures, new products, or increased business. The company itself continues to stress, that they are becoming leaner as time goes on. I believe that to be true.

Cutting Costs – The Layoffs

In 2022, Robinhood performed several rounds of lay offs. This allowed them to cut Q2 ’22 and Q3 ’22 operating expenses significantly (excl. COGS). This does not appear to have impacted their revenue growth and has given them the added benefit of being ‘right sized’. And to the best of my knowledge, no further lay offs are currently on the table. In fact, their revenue is now higher than it has ever been since IPO at $447 million and is pushing them ever closer to profitability.

“Robinhood Is Laying Off 9% of Its Full-Time Employees”

– Wall Street Journal, Apr. 29, 2022

https://www.wsj.com/articles/robinhood-is-laying-off-9-of-its-full-time-employees-11651008879

“Robinhood Lays Off 23% of Staff as Retail Investors Fade From Platform”

– Wall Street Journal, Aug. 2, 2022

https://www.wsj.com/articles/robinhood-lays-off-23-of-staff-11659471011

2023 Road Map – 4 Catalysts

Now that we’ve talked about cost cutting, let’s take a look at the road map and see if there are opportunities for fundamental growth. I will list out 4 that I believe can have a positive impact on their business.

- Options Trading in Cash Accounts

- Margin Outside Gold

- Futures Trading

- UK Market Expansion

Lets tackle the first two on the list.

Options Trading in Cash Accounts should continue to grow their existing business. This should increase their revenue generated per user as more current customers have access to more products. Options trading is particularly popular among Robinhood’s customer demographic.

Margin Outside Gold I find personally controversial. I personally don’t believe in using margin. Regardless, it should also increase their revenue generated per user.

While both of these are improvements that could turn the company profitable for EPS. They are already having a significant impact on Robinhood’s revenue as evident by their earnings reports.

Futures trading would open an entire new market for the Robinhood user and could be just as consequential, if not more so. I believe it is an incredibly potent catalyst for their user base and will allow their customers to trade more often and in new ways.

Robinhood advancing offerings for active traders

https://s28.q4cdn.com/948876185/files/doc_financials/2023/q1/Q1-2023-Robinhood-Exhibit-99-1.pdf

- In March, we applied for a Futures Commission Merchant license and, if approved on a typical timeline, we

expect to launch futures trading by the end of 2023.

UK Market Expansion should allow them to acquire a significant number of new users.

Robinhood continues to explore growth opportunities, expands access globally

https://s28.q4cdn.com/948876185/files/doc_financials/2023/q1/Q1-2023-Robinhood-Exhibit-99-1.pdf

- With an experienced team leading and an existing license in place, we believe we’re on track for our

ambitious goal of launching brokerage services in the UK by the end of the year.

To summarize, I believe expanding into a new country, the UK, and providing futures trading to their existing customers they expand their business significantly over time.

Lets take a look now at the charts and see what we can find in the price action.

Charting A Path

The first thing of note on Robinhood’s stock chart is that a series of higher lows have been put in. The price action, for the first time since IPO, is showing an increasing pattern in the price. I believe the stock has a classic Falling Wedge which I interpret as bullish. I believe the wedge has formed because of the positive developments in the balance sheet, cost cutting, and the future outlook.

Examining the MACD on the 1D time scale we also see higher lows put in as well as an MACD crossover onto the positive scale. Overall, I read the charts as having increasingly positive momentum. I also believe that momentum is growing, albeit slowly.

Lastly, on the 2D time scale my favorite indicator, DMI, shows the bulls having taken control on ~May 24 2023. I don’t think it’s any coincidence that was the low after the most recent earnings report. I believe the majority of the bears have left the stock as evident by their strength at ~11.5. We also have seen the natural termination of the ADX which implies, to me, that the previous trading trend for the stock has come to an end. A new trend does appear to be forming. It could fizzle out, but that’s up to Robinhood’s management.

I believe all of the necessary setups are currently there for them to succeed as both a company and a stock.

Closing Thoughts & Possible Risks

The Demographic & The Controversy

By discussing Robinhood here, I feel that I must mention reddit’s r/wallstreetbets. The community there has a significant impact I believe on Robinhood’s success or failure.

The community has a significant following and many of their members use the app. I believe they are an opportunity for Robinhood as well as a possible risk. The 14 million members are potential customers for the Futures trading introduction as well as the increased margin offerings.

However, the community has aligned itself with being against the Robinhood app and have been in a ‘boycott’ of the app since the $GME trading saga of early 2021. While the community is very vocal on the matter, many of the posts continue to show use of the Robinhood app. At a minimum, it remains controversial, but still in use.

This has led me to believe that most of the drama has faded and because of the high quality product Robinhood offers, has started to draw users back to the app. I believe this is well illustrated in their MAU and NFA graphs. There’s a unique opportunity here for them to either win back this community or lose them forever.

This could also be related to the flurry of trading activity seen in stocks related to AI in the past few months.

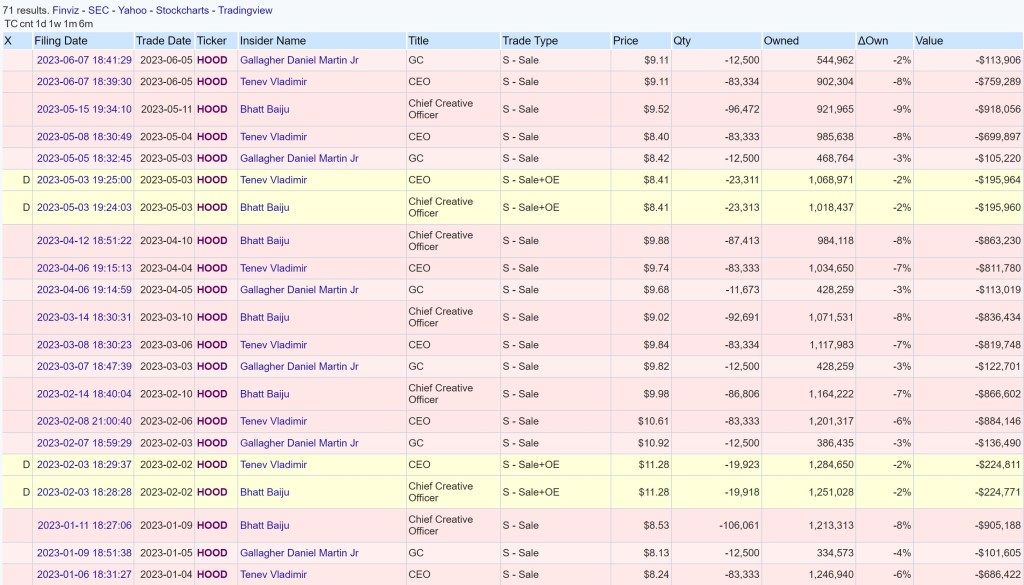

Heavy Insider Selling

An additional risk is that the insiders, specifically Tenev Vladimir, CEO & Bhatt Baiju, Chief Creative Officer, continue to sell large numbers of shares. This is creating an immense downward pressure on the stock price. If this pattern continues, it could contribute negatively to the stocks performance.

However, I believe that’s a non-issue if the company becomes profitable. I hope that we are approaching the end of the insider selling.

Crypto & SEC Action

Additionally, due to recent events, Robinhood has pulled 3 of their crypto offerings. I believe this is another mixed risk. While they will take a revenue hit by delisting those tokens, they may end up gaining users if customers of Coinbase or Binance decide to take their business elsewhere. It could end up being beneficial to Robinhood, but there’s no way of knowing at this time.

At the time of this writing there has been no report that I can find of Robinhood receiving a notice on the matters affecting Binance and Coinbase. Robinhood instead chose to remove the 3 affected securities voluntarily.

I believe this is the responsible thing to do and well advised. By taking pre-emptive action they are protecting their business from getting entangled in the matter and remaining compliant with the SEC. This is a value the company has stated a number of times during their earnings calls. I believe their actions demonstrate that value and is representative of good governance from the company leadership.

That said, the SEC could still take action against the company if they choose to do so. Therefore, it still carries some risk and must be considered.

Macro & Last Thoughts

So, here we are. It’s June 11th, 2023. Costs are significantly reduced and being controlled, notable Roadmap 2023 objectives are close, plans for new markets and offerings are approaching, and revenue continues to grow. The company is just a few pennies away on EPS from breaking even or potentially turning a profit. There is also significant distance from the drama surrounding GameStop, Robinhood, and WallStreetBets.

The charts are showing higher lows being put in place. More positive momentum looks to be coming into the stock via the MACD. Additionally, the bulls appear to have taken control via the DMI on ~May 24th, 2023.

I believe this is a case where a significant breakout could occur. It remains to be seen if it will, but I believe there is a potential trade here to the upside. It is not without downside risk though and that must be taken into consideration.

Current thinking in the market is that we may be entering a new bull market based off of recent SP500 closing levels. However, the macroeconomic picture still remains unclear. Particularly in regards to inflation, interest rates, and consumer spending.

If it is a new bull market, Robinhood may benefit from increased trading activity, but if the macroeconomic picture deteriorates it could degrade Robinhood’s business and affect the stock.

Either way, I personally believe the stock is in an interesting position within the market.

Trade carefully, trade wisely.

~Kryptonite

As always, please consult the appropriate professionals for any financial decisions. I am not a professional. I am an amateur hobbyist. These are my own personal opinions that I’ve expressed regarding the market and the companies mentioned above. I am not responsible for any decision, trade, or investment you may make. Please see my Disclaimer

You should assume that as of the publication date of any report, post, or communication referencing any publicly traded security or asset that Kryptonite Research (myself) may have a position in the security or asset and I might stand to realize significant gains if the price of the stock moves. Following publication of any report, post, or communication, I intend to continue transacting in the securities covered therein, and Kryptonite Research (myself) may be long, short, or even neutral at any time thereafter regardless of Kryptonite Research’s (myself) initial position. I reserve the right to alter my position at any time without notice.

Images are sourced from the TradingView app, Adobe Stock photos, and Robinhood’s Investor Relations. I do not claim ownership.

As an additional disclaimer, at the time of this writing I am a Robinhood customer and holding a position in Robinhood’s stock.

https://www.tradingview.com/symbols/NASDAQ-HOOD/financials-overview/

https://investors.robinhood.com/financials/quarterly-results/

https://www.reddit.com/r/wallstreetbets/

https://www.tradingview.com/symbols/NYSE-SCHW/financials-overview/